Winter 2017

U.S.-Mexico Energy and Climate Collaboration

What is the outlook for cross-border collaboration on key energy issues?

Four years ago, as the administration of Enrique Peña Nieto began, the Wilson Center’s Mexico Institute outlined a number of areas in which productive collaboration could take place between the Mexican and U.S. governments. Those areas focused on non-oil related energy issues for an obvious reason: at the time, Mexico’s oil and gas sector remained closed to private and foreign investment, and collaboration in this area was stifled at best.

The constitutional reforms of December 2013 (and the implementing legislation of the following year) changed this scenario dramatically and profoundly. A full opening of the hydrocarbons value chain to private and foreign investment, and the gradual construction of a competitiveness marketplace for energy suppliers have revolutionized the Mexican energy model. This is not just the case in oil and gas, of course: the electricity sector too has been extensively liberalized, and 2016 saw two major generation auctions successfully carried out by the government. There has been impressive progress in developing Mexico’s renewable energy potential — and remarkably, given the expected expansion of its hydrocarbons sector, ongoing commitments to limit carbon gas emissions.

Mexico’s energy sector and the energy relationship between Mexico and the United States have experienced notable progress over the past four years. But looking to the future, there are even more meaningful paths for collaboration in light of the transformation of energy systems worldwide, the opportunities presented by Mexico’s liberalized energy sector, and the Trump administration’s noted interest in energy. The existing North American energy dialogue has become a critical resource in preparing for the future of global and regional energy markets, and it is worth a full examination.

Why Energy Matters

Energy is a major component of both the U.S. and the Mexican economies, responsible for wealth creation, innovation, and employment. Across both countries, millions of people work in the traditional energy sector, and millions more are finding work in the areas of renewable energy and energy efficiency. But secure access to comparatively low-priced energy is also crucial for economic competitiveness. Prior to Mexico’s energy reform, high prices for industrial consumers of electricity compromised its manufacturing competitiveness, and natural gas shortages meant repeated stoppages at factories in the north of the country. Since the reform was passed, prices have been reduced dramatically in Mexico, falling by between 21 percent and 30 percent for industrial consumers between September 2014 and September 2015. This has significantly improved the economic competitiveness of Mexican manufacturers.

Mexico’s New Energy Model

After 75 years of running a closed and monopolistic energy sector, in December 2013 the Mexican government won congressional approval for a far-reaching reform package that liberalized both the hydrocarbon and electricity sectors. This paradigm shift happened in the face of considerable opposition from left-wing parties and nationalists, but the Peña Nieto government was still able to win a two-thirds majority in both chambers of Congress and approval from a majority of the state legislatures. Over the next two years, implementing legislation was passed by Congress, and regulatory frameworks and organisms have been constructed.

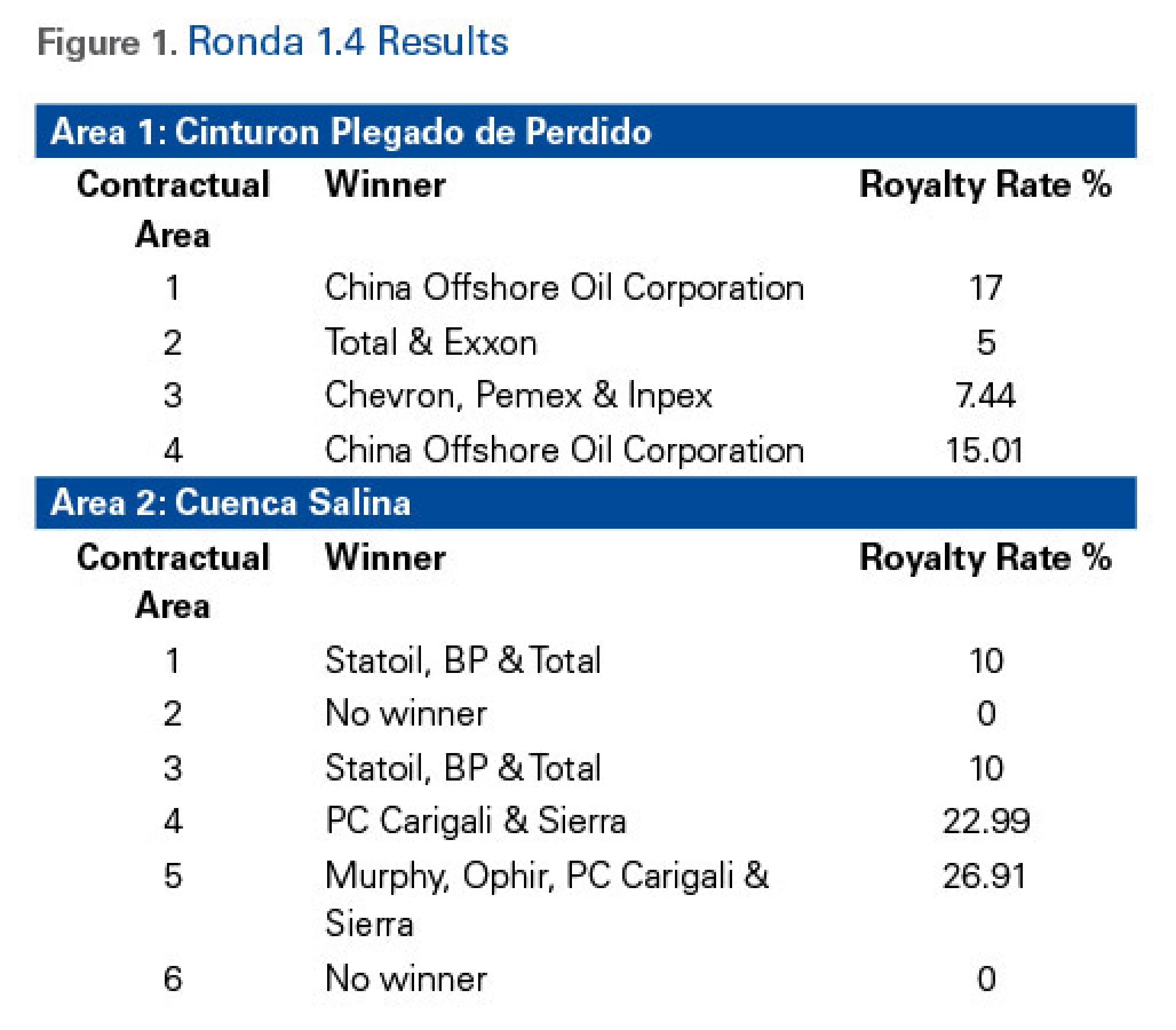

In December 2014, Energy Secretary Pedro Joaquin Coldwell announced the nation’s first oil bidding round (Ronda 1) since 1938, and over the following two years successful auctions were held for shallow- and deepwater fields and for onshore blocks. Although the first of these auctions (Ronda 1.1), in July 2015, was a disappointment with only 2 out of 14 blocks awarded, the National Hydrocarbons Commission (CNH) and Energy Ministry (SENER) listened to investor feedback and changed the process for subsequent auctions, to impressive effect. In Ronda 1.2, 3 out of 5 blocks were allocated, with impressive winning bids ensuring higher than expected revenue for the government, and Ronda 1.3 saw all 25 available blocks awarded. The “jewel in the crown” of Ronda 1, however, came in December 2016, one year after the completion of Ronda 1.3, and three years after the signing of the constitutional reform. In this auction, the CNH successfully allocated 8 out of 10 available fields, with the winning bids coming in with royalty commitments far above the levels expected by the government (figure 1). On the same day as Ronda 1.4, the CNH also oversaw the bidding process for the historic Trion Deepwater field farm-out, in which firms competed to partner with Mexico’s state-owned Pemex petroleum company in an existing field in the Perdido Fold Belt, in the Gulf of Mexico near the U.S.-Mexico border. In total, the first bidding round of the new hydrocarbons model saw the signing of 39 contracts and is expected to generate $49 billion.

Figure 1. Ronda 1.4 Results

The success of this extraordinary change in Mexico’s hydrocarbons industry was brought about in large part by the willingness of the Mexican government to engage in dialogue with the investor community. When Energy Secretary Pedro Joaquin Coldwell announced the Ronda 1 terms in December 2014, he declared that the government was open to feedback from the private sector and foreign investors to be able to improve on the investment climate. Although this may be seen as standard practice in other jurisdictions, in Mexico this marked a dramatic departure from the traditional, state-imposed reality in the hydrocarbons sector. Not only did Mexico welcome foreign investment, it invited the investors to help shape the rules of the new system.

Mexico’s petroleum markets are also being revolutionized downstream. Beginning in January 2016, private companies are now allowed to compete with Pemex in the retail market and, in April 2016, private companies were allowed to import refined products without having to go through Pemex. This liberalization of the refined products market has seen enormous interest from foreign oil companies, with Gulf already opening its first gasoline stations in the country in mid-2016. Lastly, 2017 will see the partial liberalization of gasoline prices in Mexico, which has brought a consumer backlash as prices have risen dramatically.

However, significant challenges still remain for Mexico’s hydrocarbons sector. Pemex continues to face enormous financial pressure due to an overwhelming government tax burden, crippling labor liabilities and dramatically reduced revenues due to falling production and low international oil prices. Pemex’s production decline has been profound and dramatic, falling from 3.4 million barrels per day in 2004 to less than 2 million per day in 2017. Pemex has also been hemorrhaging money on its downstream operations: its six refineries have been operating at only 66 percent capacity over the past few years, and it is estimated that they result in a US$9 billion loss every year for the company. This also means that Mexico has been importing record supplies of gasoline, reaching 867,000 barrels per day in July 2016.

Nonetheless, Pemex is finally beginning to adapt to the new environment. In February 2016, the company brought in a new CEO, Jose Antonio Gonzalez Anaya, who has committed to partnering with the private sector. The proof of this commitment came in December 2016, when Pemex not only participated in a winning consortium in December 2016 for a deep-water block in the Perdido Belt in Round 1.4, but also entered an association within the Trion field through a farm-out. The winning bidder in the farm-out process, Australia’s BHP Billiton, not only ushered in a new era of collaboration for Pemex but also brought a $624 million cash payment for the company, a welcome injection at the end of what had been a very difficult year. These events suggest that change is coming fast for Pemex, and that there is significant reason to be optimistic about the future.

At the same time as this extraordinary process was unfolding, Mexico was continuing to transform its natural gas sector. During 2011 and 2012, the country had experienced severe natural gas shortages, with industrial consumers being cut off from supplies at critical moments, compromising their ability to meet orders. Building on existing commitments, the Peña Nieto administration has continued to expand Mexico’s natural gas pipeline network, and even more important, has overseen new cross-border pipeline projects that have brought much needed low-cost gas in from the United States.

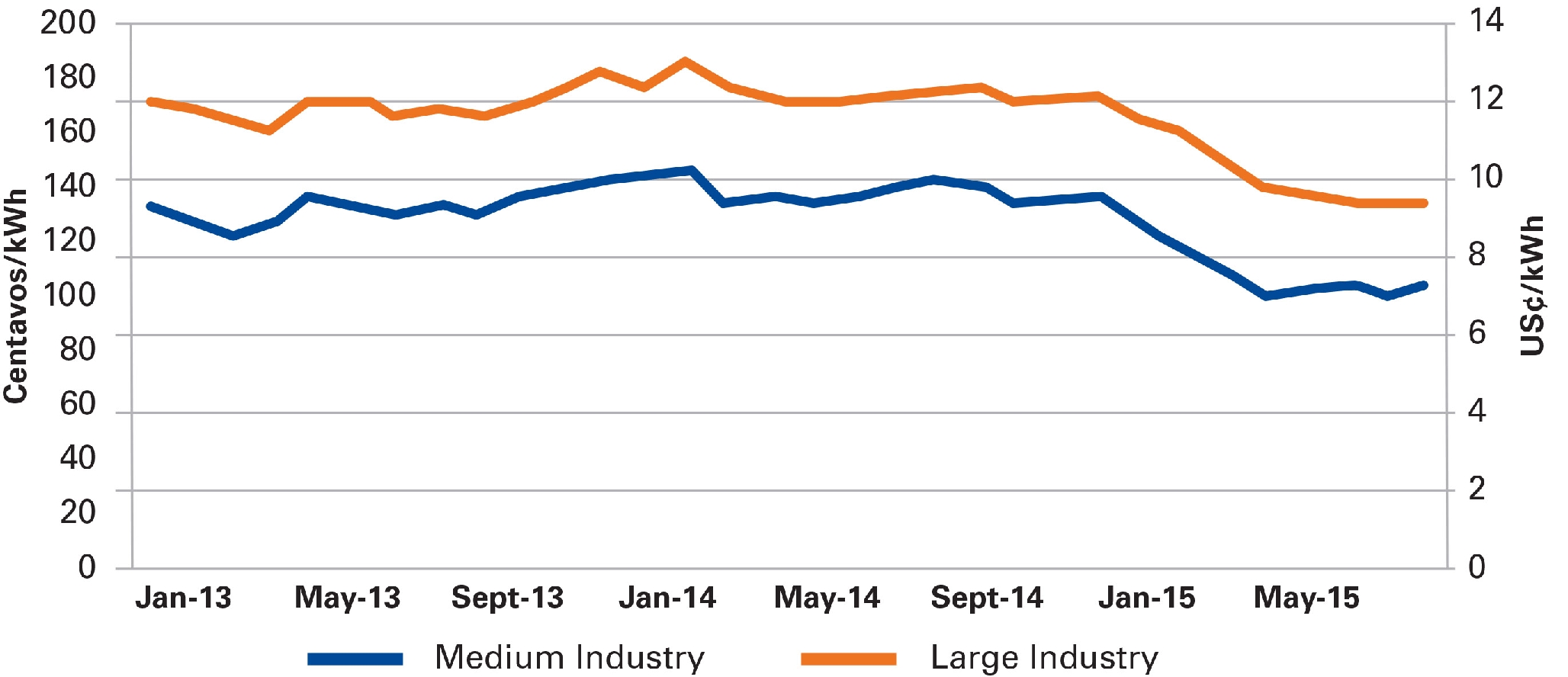

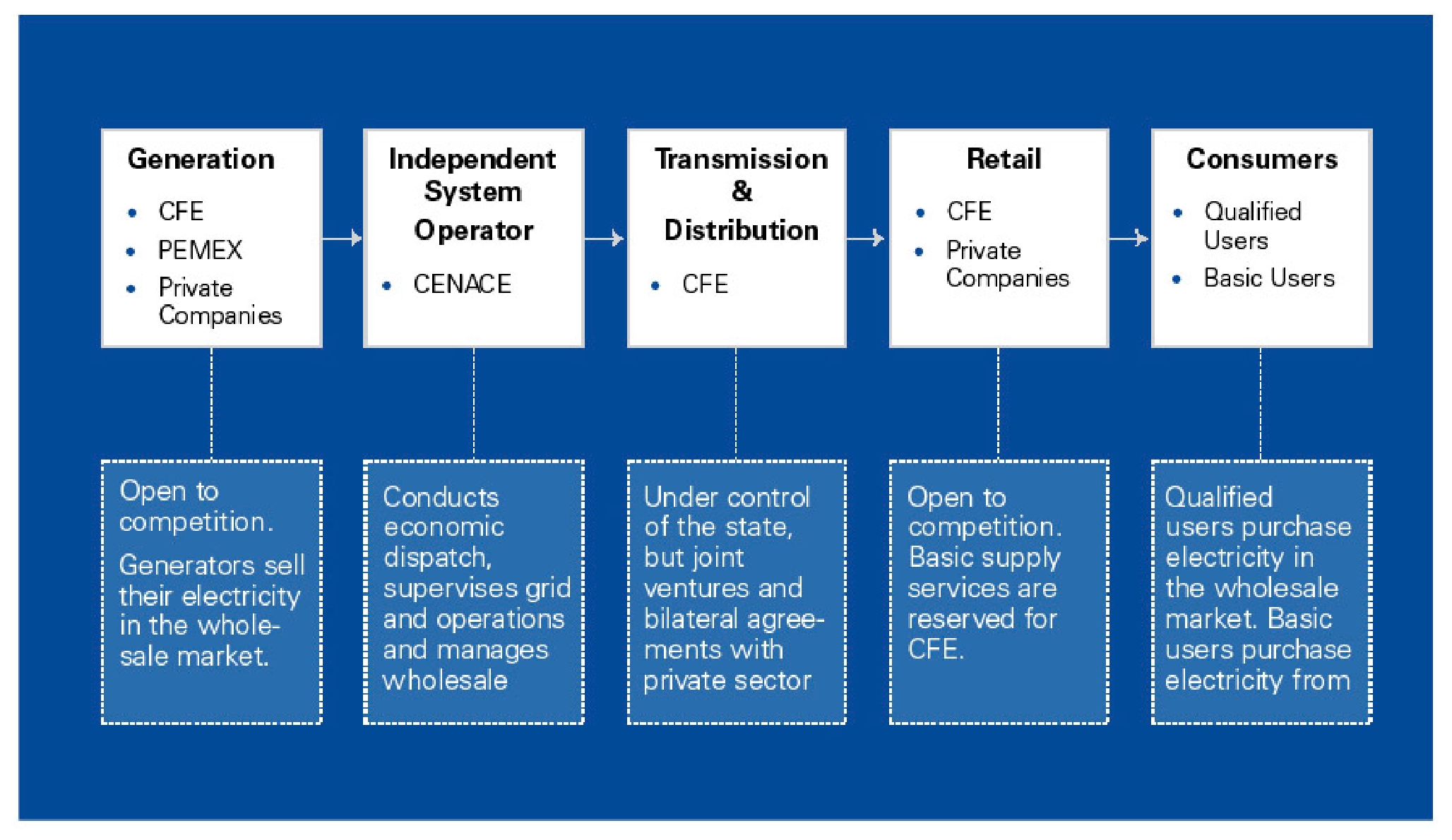

The influx of natural gas into Mexico is also helping to transform the electricity system (figures 2 amd 3). As with the hydrocarbons industry, Mexico’s power sector has been completely opened up to competition thanks to the 2013 constitutional reform. Before the reform, the power sector was dominated by the state-owned utility, the Comision Federal de Electricidad (CFE), a monopolistic system that only allowed private power generation under certain conditions. The electricity reform helped decentralized the previously state-owned and vertically integrated industry, permitted private investment, made power generation more competitive, created an independent body (the CENACE) to run the wholesale electricity market, and guaranteed open power grid access for all participants. The transformation also affected the CFE. It was unbundled, split into several companies that will compete with each other and with private firms.

Access to stable supplies of natural gas in Mexico is transforming generating capacity. It is estimated that 44 percent of generation capacity additions up to 2029 will be natural gas–based, and a number of existing fuel oil–powered plants will be converted to gas.

Figure 2. Mexico’s Industrial Power Prices

The importance of the power sector reforms was made clear by Mexico’s energy minister, Pedro Joaquin Coldwell, when he called it “the economic competitiveness reform.” As Alejandro Chanona Robles has argued, “access to reliable and affordable power can give businesses a competitive edge over their rivals, stimulate job creation and spur economic growth. . . . Studies suggest that cheaper electricity can substantially boost Mexico’s manufacturing base.”

Figure 3. Mexico’s New Power Sector Structure

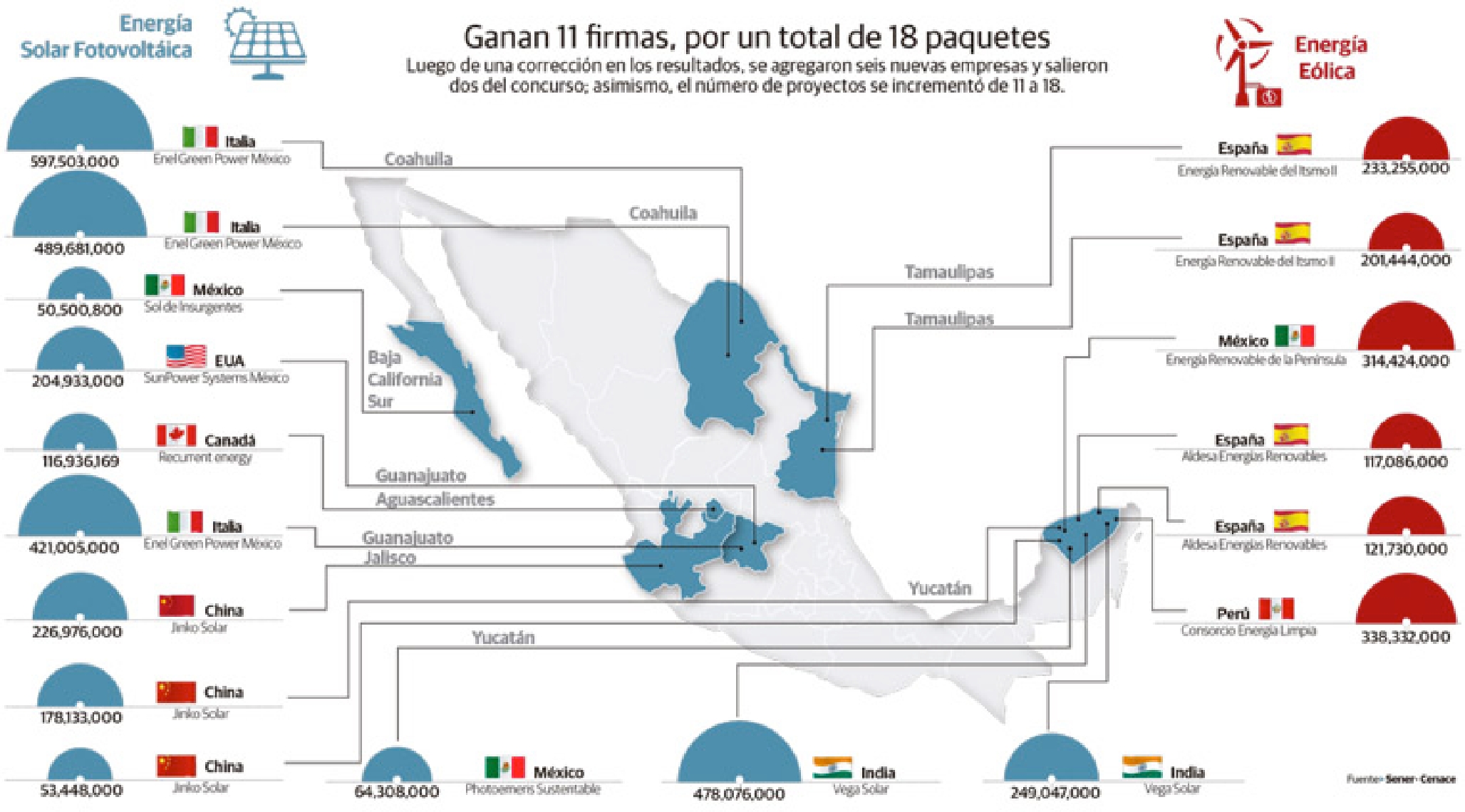

But Mexico’s power sector transformation has also already brought significant investment in new renewable energy capacity. In March 2016, the first electricity generation auction was held, with 18 renewable power contracts awarded, attracting record-low prices per megawatt (MW) of power generated (figure 4). A second auction in September saw even lower prices guaranteed.

Figure 4. Mexico’s First Renewable Energy Auction, 2016

Source: AWS True Power

Further changes will follow in Mexico’s power markets, with an opening of the capacity market in February 2017 and the launch of a market for clean energy certificates in 2018. This latter initiative will cement the government’s already impressive commitment to reducing carbon emissions and boosting renewable energy production in Mexico.

The Liberation of the U.S.-Mexico Energy Dialogue

For decades, Mexican sensitivities regarding the connection between energy and national sovereignty prevented the development of a modern and multifaceted dialogue over energy cooperation between the two countries. The 2013 reform, however, opened the way for comprehensive interaction on energy policy. In February 2014, only two months after the reform was approved, the three North American heads of government met in Toluca, in the State of Mexico, to discuss the future of regional integration. Energy featured high on the agenda, and it was agreed that the energy ministers of the three countries would begin a regular dialogue. The first meeting took place in Washington, D.C., in December 2014, and agreeed on an agenda for cooperation on three specific points:

Publicly available collaboration on North American energy data, statistics, and mapping; Responsible and sustainable best practices for unconventional oil and gas developments; and a modern, resilient energy infrastructure for North America, including policies, regulations, workforce, innovation, energy efficiency practices, and sustainable technologies.

The breadth of this agenda helps to emphasize the potential for collaboration now that the Mexican energy system has been transformed. The memorandum of understanding signed by the energy minsters institutionalized an information-sharing framework for participants to promote dialogue and cooperation. Under the North American Cooperation on Energy Information initiative (NACEI), the three ministers agreed to set up a working group that would facilitate this coordination, combining the efforts of the three countries’ energy departments and information agencies, statistics and census bureaus, and national energy control and regulatory boards. The group was specifically tasked with comparing, validating, and improving respective energy import and export information; sharing publicly available geospatial information on energy infrastructure; exchanging views and information on cross-border energy flows; and harmonizing terminology, concepts, and definitions of energy products.

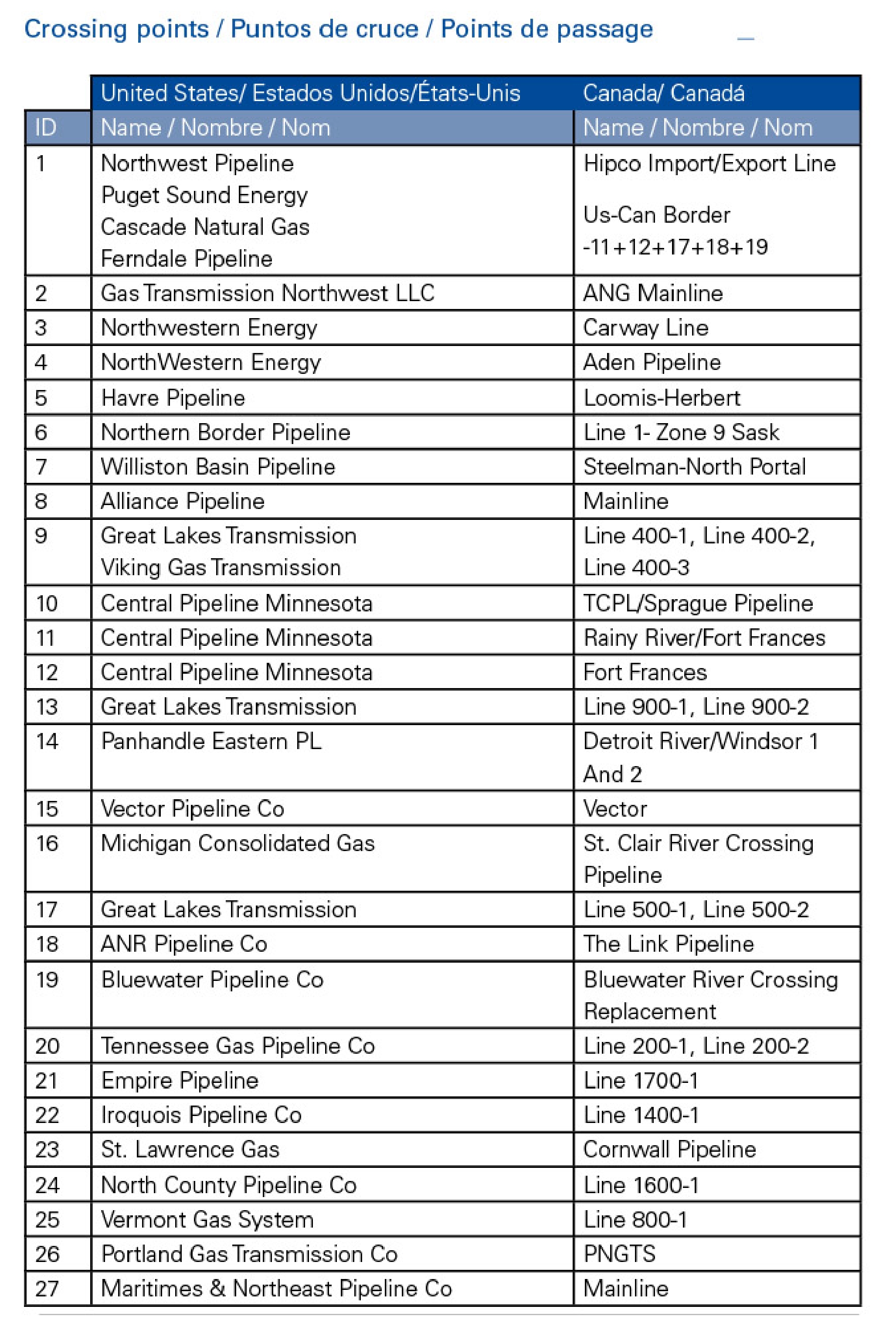

Figure 5. Border Crossings of Natural Gas Pipelines

The leadership role played by the United States in this regional approach was underlined by the 2015 Quadrennial Energy Review (QER), which focused extensively on the opportunities for energy cooperation in North America. The QER chapter on North America concluded that the United States has significant energy trade with Canada ($140 billion per year) and Mexico ($65 billion), yet greater coordination is needed to improve energy system efficiency and build resiliency against disruptions of the North American energy market, data exchanges, and regulatory harmonization.

In 2015, the U.S. Energy Information Administration (EIA), Canada’s National Energy Board, and Mexico’s Secretaría de Energía (SENER) produced a Trilateral Energy Outlook. This report established projections for crude oil, refined products, and natural gas and electricity markets across the region to 2029. Although the report’s authors emphasize that “it does not reflect results of an integrated North American energy model” nor should it “be construed as an official outlook for any of the Trilateral members,” there is, for the first time, the possibility of a more holistic approach to planning the future of North America’s energy sector.

The December 2014 meeting of the energy ministers was followed in May 2015 by a meeting on the margins of the Energy and Climate Partnership of the Americas and the Clean Energy ministerial meetings in Mérida, Mexico. The three ministers agreed to form a new Working Group on Climate Change and Energy, involving regular interactions between teams from all three countries. The agenda that was laid out in Mérida included reliable, resilient, and low-carbon electricity grids; more focus on clean energy and energy efficiency, including energy management systems; carbon capture, use, and storage; climate change adaptation and resilience; and oil and gas sector emissions, including methane and black carbon.

The energy ministers praised the new initiative. Mexico’s Pedro Joaquin Coldwell emphasized that its agenda demonstrated a commitment to “a path to achieve deep de-carbonization.” The United States’ Ernest Moniz emphasized the initiative’s potential for “facilitating cooperation to deploy innovative renewable energy technologies, modernize the grid, and increase energy efficiency to combat climate change and reach greenhouse gas targets while growing low-carbon economies in North America.”

This institutionalization of a regional energy and climate agenda is a prerequisite for meaningful and sustained cooperation. Building on the experience of the North American Energy Working Group (NAEWG) in the early 2000s, the new working group will coordinate its efforts through socialization and harmonization. The first process has already shown its value: the meetings of the three energy policy representatives have encouraged mutual understanding and increased interaction between their ministries. The second process will take longer, and we should not expect it to be a linear or an even process. It makes more sense to harmonize regulations and standards in some areas than in others, and sometimes the harmonization should be bilateral rather than trilateral. In most areas, the goal should be compatibility and coordination rather than full homogenization.

Another area that has progressed impressively since 2013 has been regulatory cooperation. As Mexico has opened its sector to private participation, its regulatory agencies have been strengthened and their power expanded. The CNH has been charged with running the bidding process for oil blocks in Rounds 1 and 2, and the Comision Reguladora de Energia (CRE) has overseen both the opening of the electricity market alongside SENER and the CENACE, and the regulation of transportation, storage, and distribution of hydrocarbons, including natural gas. Furthermore, the reforms created a new environmental regulatory agency, the Agencia de Seguridad, Energia y Ambiente (ASEA), to oversee the industrial safety and environmental protection aspects of the hydrocarbons sector. Operating under the control of the environmental ministry (SEMARNAT), the ASEA has had to progress rapidly since its inception in 2015. In fact, all three regulatory agencies have had to adapt to dramatically altered circumstances during the first three years of Mexico’s new energy model. To do so, they have made a concerted effort to acquaint themselves with international best practices, and Mexican contact with U.S. and Canadian regulators has been an integral part of that process. Regulatory exchanges with California and Texas (and Alberta) have been particularly significant, as have exchanges with U.S. federal organizations such as the Bureau of Safety and Environmental Enforcement, the Bureau of Ocean Energy Management, the Bureau of Land Management, the Environmental Protection Agency, the Federal Energy Regulatory Commission, and the Pipeline and Hazardous Materials Safety Administration.

U.S.-Mexico Climate Cooperation

Mexico has long been recognized as an emerging market leader in international climate change negotiations. Beginning with the presidency of Felipe Calderón, Mexico has attempted to develop an aggressive approach to global climate talks that is backed up by progress on climate mitigation and renewable energy policy at home. President Peña Nieto’s continuation of this policy surprised some who had predicted a hydrocarbons-friendly approach, and has even strengthened Mexico’s global climate position by securing legislation in Mexico’s Congress for a 50 percent reduction in carbon emissions by 2050, alongside ambitious targets for electricity generation from renewable sources. Mexico was also the first developing country to declare its Intended Nationally Determined Contribution for greenhouse gas reductions under the Paris Accord process in April 2015, and has undertaken a commitment to reduce its black carbon emissions by 51 percent by 2030. Largely thanks to this commitment, Mexico and the United States became partners in pushing the Paris Accord in December 2015, setting the stage for further regional cooperation.

The North American energy dialogue has been an important force driving cooperation on climate issues. In July 2016, at the Ottawa North American Leaders’ Summit, Mexico agreed to join the existing U.S.-Canada agreement on methane emissions reductions. The trilateral accord commits the countries to reducing methane emissions from the hydrocarbons industry by up to 45 percent by 2025. Mexico had previously resisted a commitment to reduce its emissions, partly because of opposition from Pemex and partly because of the energy reform’s already overwhelming agenda. Alongside pressure from the Canadian and U.S. governments, extensive efforts by civil society groups, including the Environmental Defense Fund (EDF) to promote the emissions reductions were successful in convincing the Peña Nieto administration of the importance of a trilateral accord. The EDF, quoting Mexican government figures, estimate that methane emissions from the hydrocarbon industry make up 19 percent of total methane emissions in the country. Trilateral cooperation can also be credited with 2016’s most important global climate accord, the Kigali Agreement on phasing out hydroflourocarbons (HFCs) in October. In 2009, during a meeting of the Montreal Protocol, the United States, Canada, and Mexico (plus the Maldives) pushed for international cooperation to reduce HFC emissions as a crucial component of fighting climate change.

Building a New Agenda: Regulation and Infrastructure Lead the Way

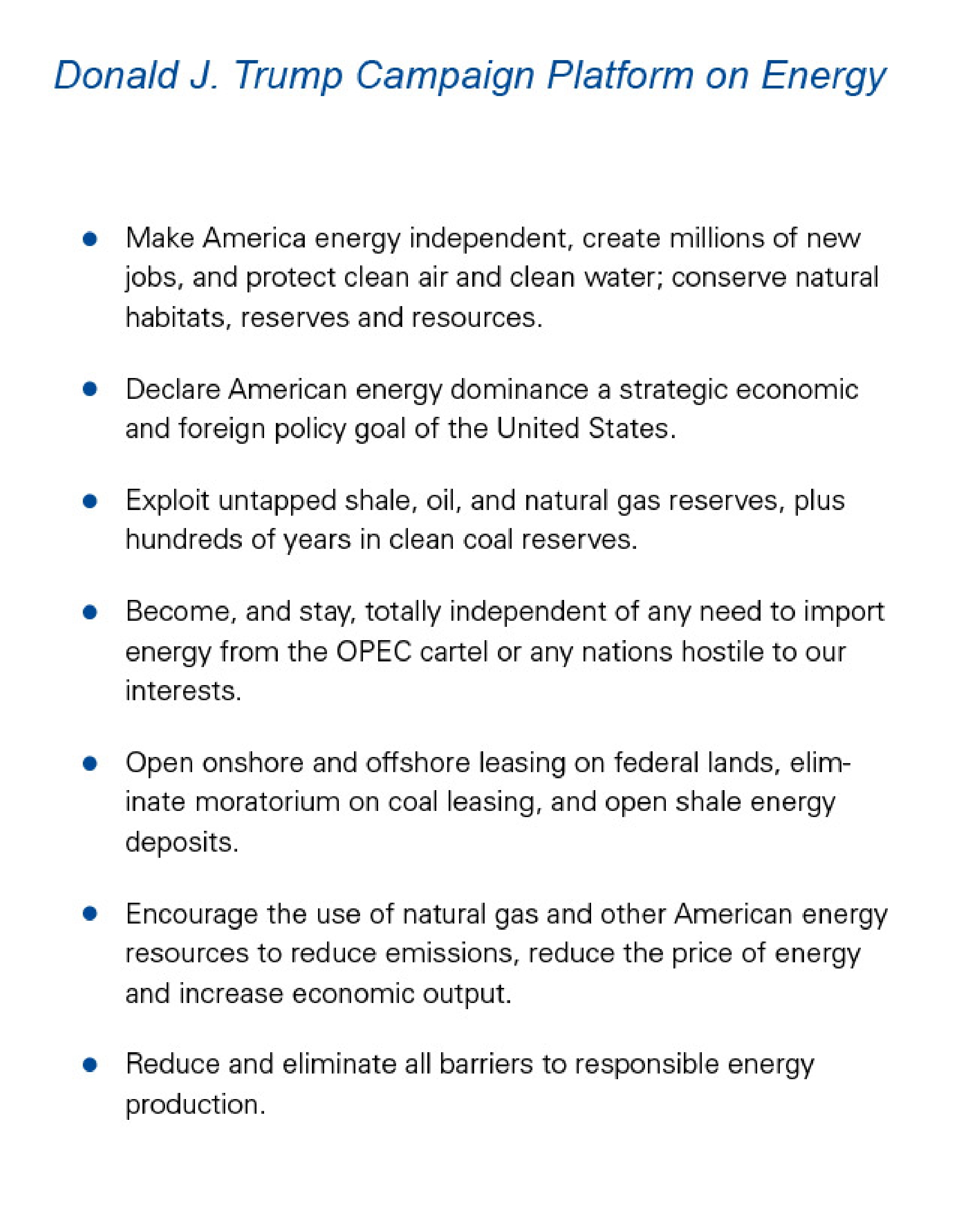

The beginning of the administration of President Donald Trump in January 2017 presents an opportunity to move the energy relationship between Mexico and the United States in exciting new directions, in addition to consolidating existing areas of agreement. Although the specifics of the new administration’s energy policy are far from clearly defined at present, four clear priorities emerged during the presidential election campaign that are likely to persist and have implications for the energy relationship with Mexico. First, the Trump campaign emphasized the need to eliminate U.S. dependence and focus on importing oil from friendly nations. The second goal is a concern with reducing the regulatory burden faced by private energy firms. Though much of this regulation takes place at the level of state agencies, it is likely that the Environmental Protection Agency will see its mandate to regulate carbon gas emissions greatly reduced. Furthermore, the appointment of former Texas governor Rick Perry as energy secretary signals a move to cut back on red tape and promote the exploitation of America’s shale, oil and natural gas reserves. Third, throughout the campaign, Trump emphasized the need to invest in U.S. infrastructure to generate jobs and improve competitiveness. This is likely to have ramifications for the energy sector. Lastly, the new administration has signaled its intent to boost the use of natural gas, both as a way of reducing emissions and lowering energy costs for the consumer.

Each of these priorities has important implications for the bilateral relationship. The first element of the Trump energy platform that has direct relevance for Mexico is the goal of becoming “totally independent of any need to import energy from the OPEC cartel or any nations hostile to our interests.” Ensuring “friendly suppliers,” such as Canada and Mexico, has long been a goal of U.S. energy policy, and Mexico stands to benefit from this. Although the new administration will seek to boost national production to ensure independence, most experts recognize that North American, rather than U.S., oil independence is a much more reasonable target at which to aim. This means that the Trump administration should recognize the importance of ensuring the long-term success of Mexico’s energy reforms.

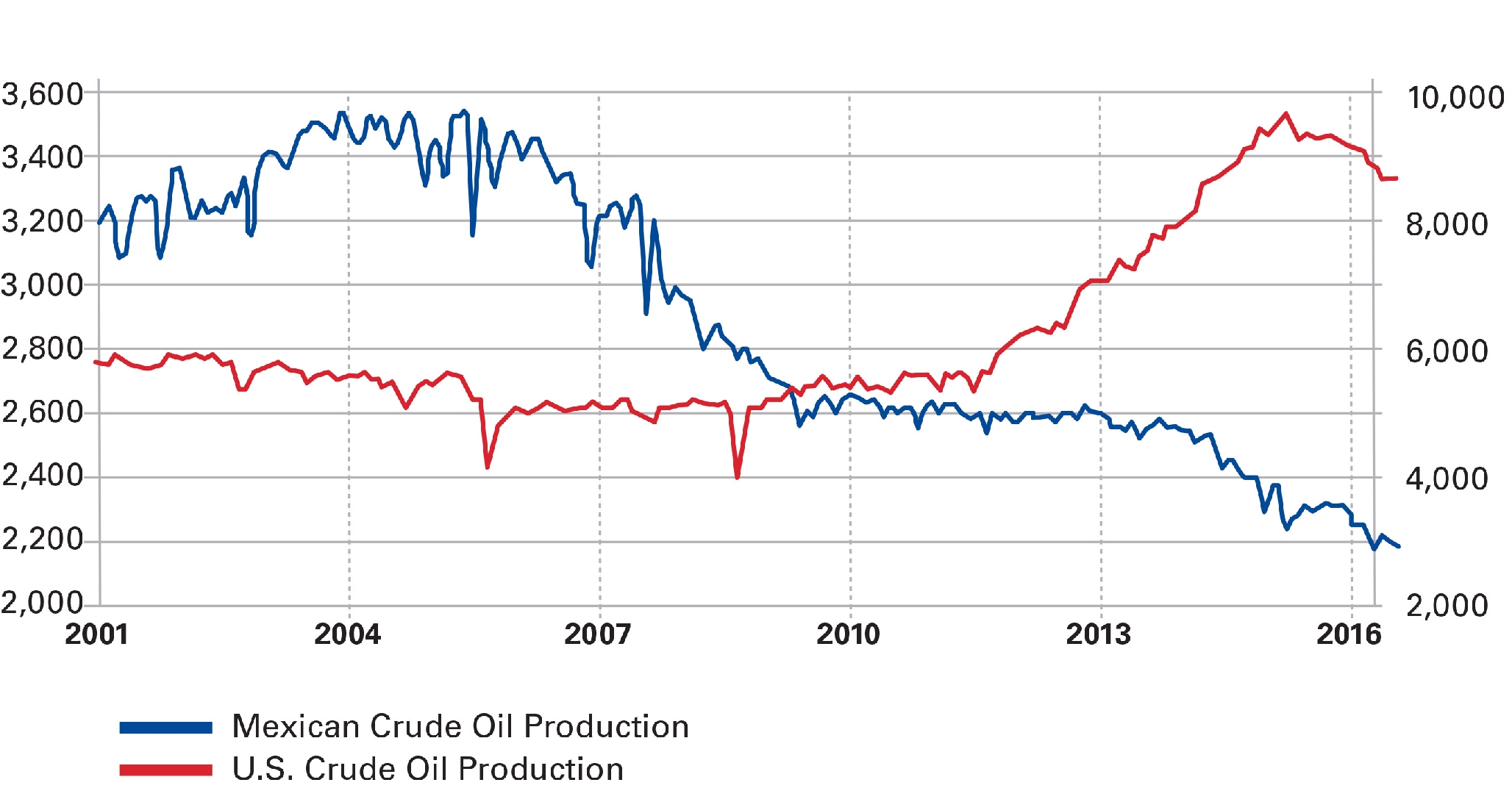

Two factors make this point particularly relevant. First, Mexico has seen a prodigious decline in oil production in recent years and the reforms are the best hope of reversing that decline (see figure 6). Secondly, the reform under attack from opposition parties in Mexico and, with the possibility of a shift to the left in the 2018 presidential election, there is a risk that the reform will stall or be rolled back. This would be an alarming prospect for both the United States and for a number of its companies that have been successful in first-round oil contract bidding.

Figure 6. Mexican vs. U.S. Oil Production, 2001–16 (thousands of barrels per day)

The second element, regulatory simplification, provides a compelling opportunity for Mexico to work with the United States to reduce the burden of its own regulatory system for energy firms. Although its regulations and regulatory bodies have seen substantial progress since the 2013 reforms, Mexico still has a regulatory system in place that seeks to prohibit, rather than facilitate, activity by the energy industry. The change of tone in Washington provides an opportunity for Mexico’s regulatory agencies to develop a dialogue with their U.S. counterparts that focuses on efficient regulation, something that the emerging private oil and gas industry is crying out for in Mexico. Critical issues concern repetitive paperwork, interagency coordination, permitting, and the use of online compliance mechanisms. If the United States is about to see a concerted push toward more efficient regulation, then it behooves Mexico to follow suit, to maintain competitiveness and to facilitate the integration of energy markets. Existing dialogue with state regulators in Texas have already emphasized the importance of a paradigm shift in Mexican regulation; the approach of the new U.S. government offers a chance to take that conversation further, in forums such as the existing North American dialogue.

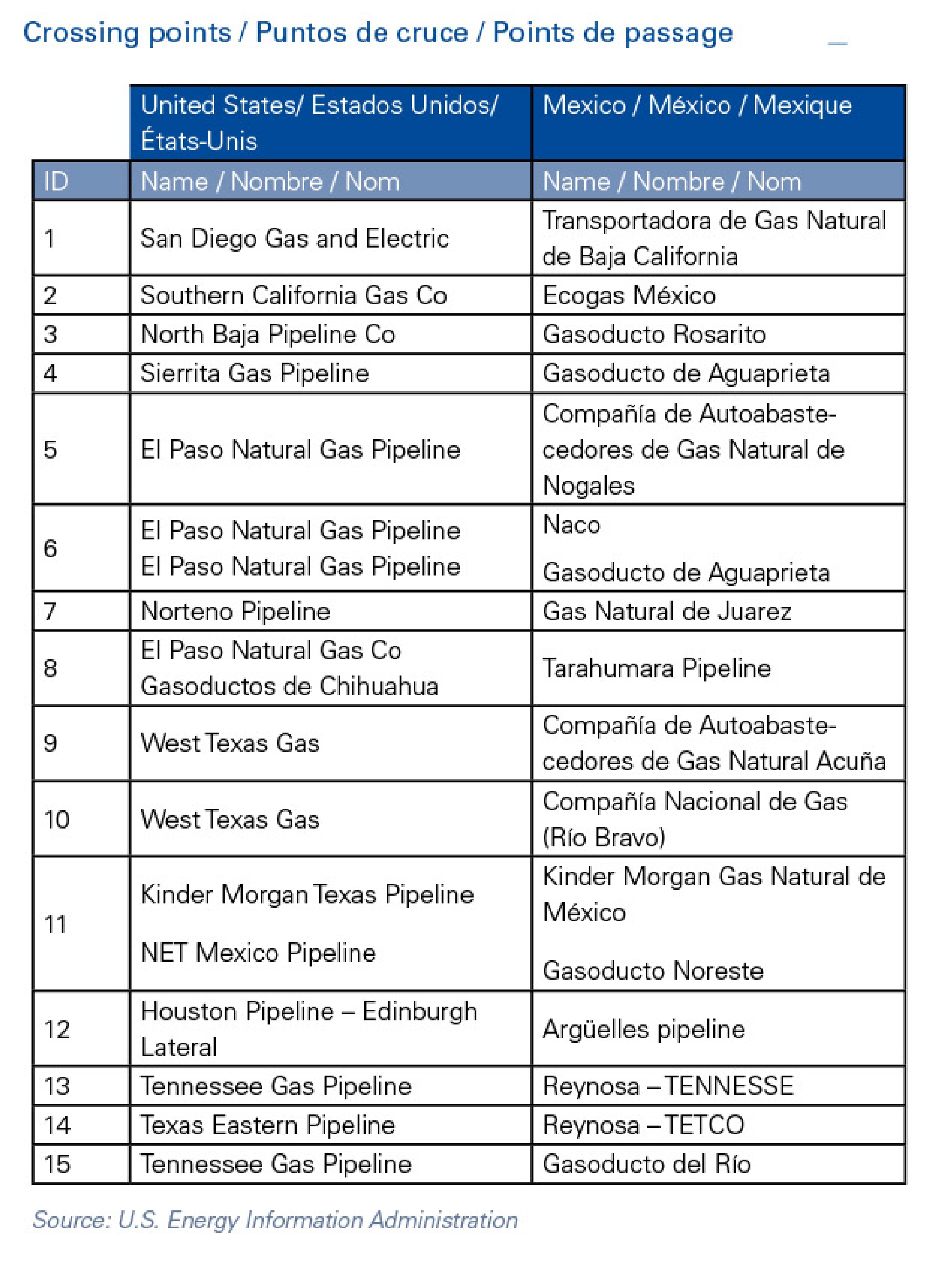

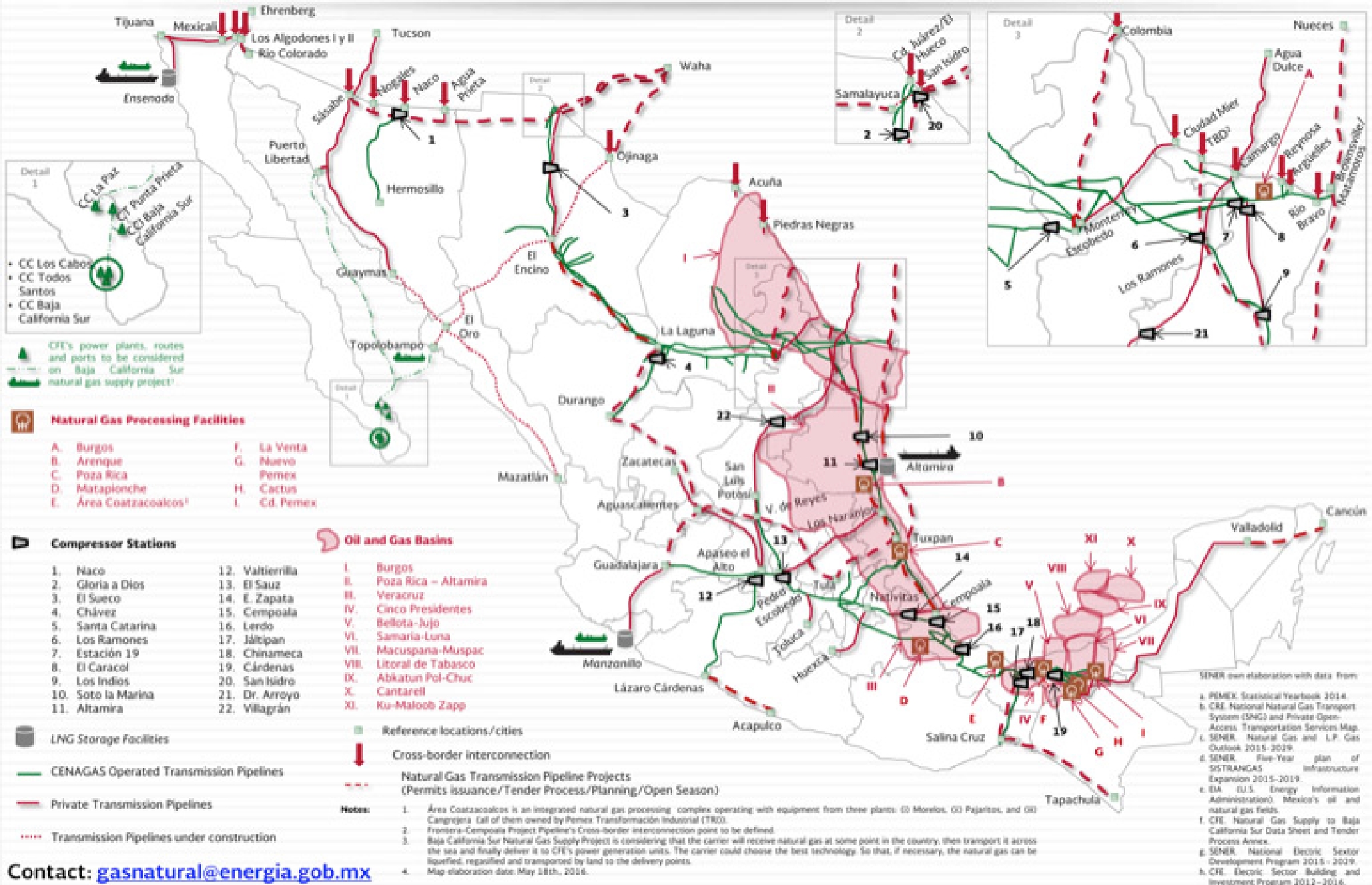

On the third energy priority, infrastructure spending, there are ample opportunities for ongoing energy infrastructure projects that take into account the increasingly integrated nature of energy markets, from oil and gas pipelines to cross-border transmission lines and a coordinated approach to refining capacity. A crucial element of the success of the Mexican energy reform has been the arrival of natural gas from the United States through cross-border pipeline projects (see figure 7). These pipelines took years to plan and build, and it is vital that future Mexican demand is considered with enough anticipation to ensure that pipeline capacity exists to carry gas to market. Mexico’s refineries are likely to see an overhaul in the next few years as Pemex seeks partners for its refining division that consistently loses around US$9 billion a year. If Mexico plans to invest in building new refining capacity, it would be wise to consider the current and future state of the U.S. refining sector, which is aging and has limited capacity.

Figure 7. U.S.-Mexico Cross-border Natural Gas Pipelines

Electricity is also ripe for cross-border cooperation. Little has been done over the past four years to increase U.S.-Mexican interconnections, with only 10 connections linking the markets of the two countries (four connections to the Western Electricity Coordinating Council and six to the Electricity Reliability Council of Texas). However, given the increase in capacity in Mexico and the rapid growth of the renewable energy industry on both sides of the border, there now exists an opportunity to plan cross-border transmission in order to benefit both producers and consumers with lower-cost and shorter-distance options for transmission. A prime example of this potential is the concept of an electricity transmission line in Mexico’s northern border states that would allow electricity to travel not only between Mexican states and across the border to U.S. consumers, but also permit electrons generated from wind energy projects in Texas to travel across the border to Mexico, move along the border, and then cross back over into California, where demand for renewable energy is growing rapidly (figure 8). In January 2017, the United States and Mexico signed a new cooperation agreement on grid reliability, setting the stage for increased connectivity between the two countries’ electricity systems.

Figure 8. Mexico’s Planned Electricity Transmission Projects

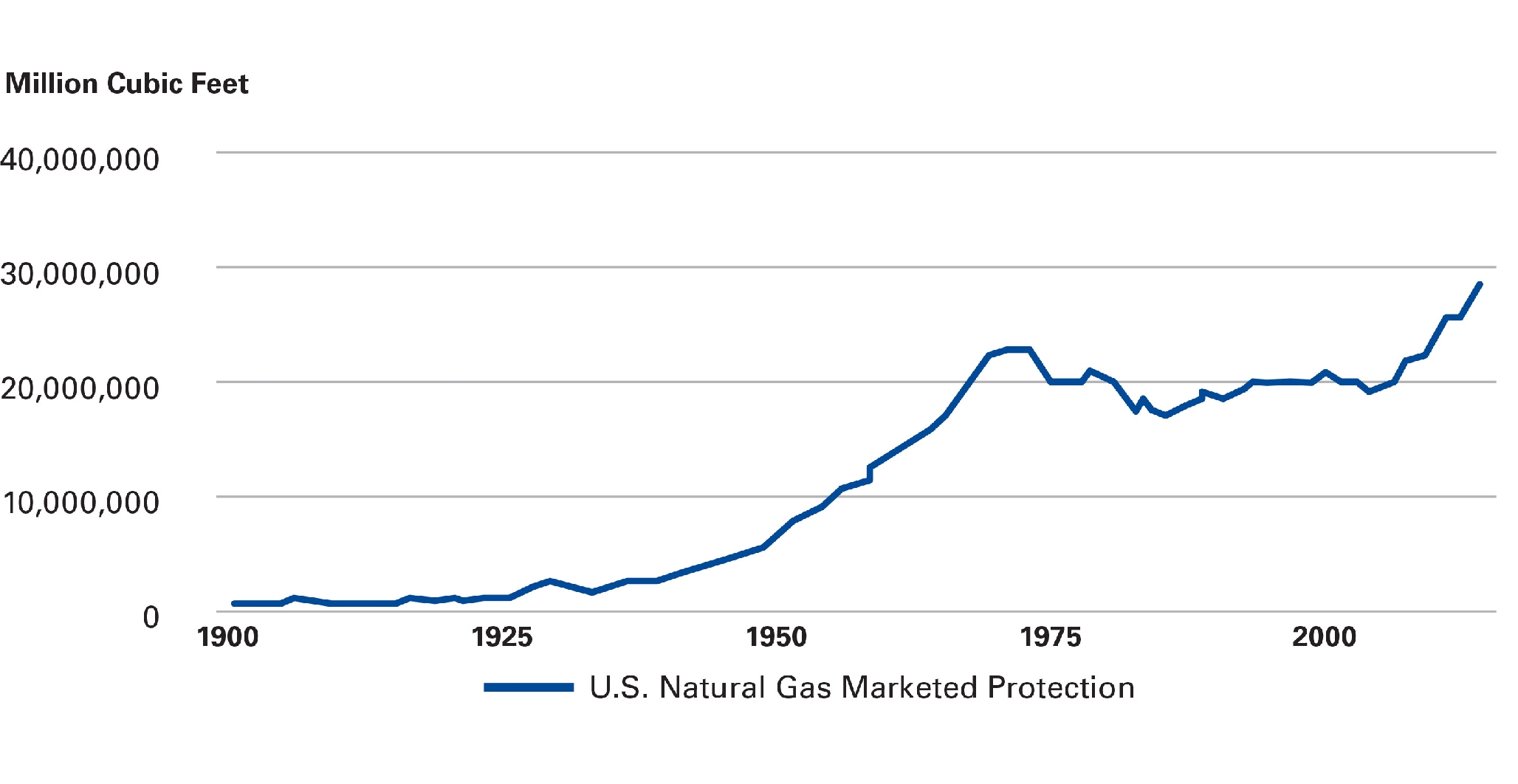

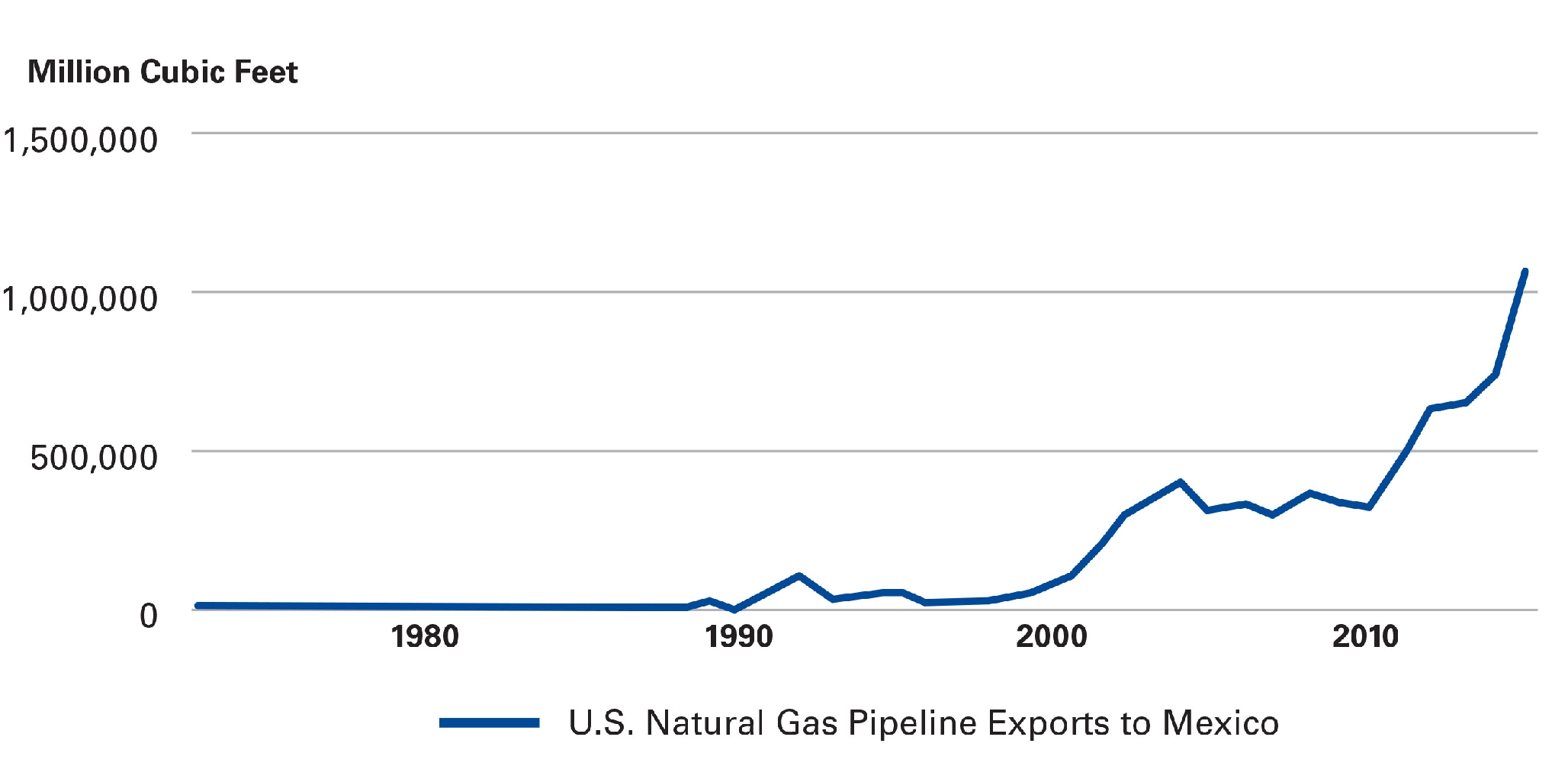

Finally, it is worth focusing on the Trump administration’s goal of boosting natural gas production and use. If gas production is to grow in the United States, new consumers will be needed to sustain a price that allows for investment in the sector. Fortunately for gas producers, it is expected that Mexico will see its demand for natural gas grow rapidly, and it is estimated that exports to Mexico will soon reach between 8 and 10 percent of U.S. production (figure 9). Mexico plans to dramatically boost its internal natural gas pipeline network over the next few years, and it is expected to grow more than 90 percent before the end of the decade. In addition to satisfying demand in Mexico, in the long term there is the opportunity to export U.S. natural gas via pipeline to Central America and through liquid natural gas facilities built along the Mexican coast. Although this could also, of course, be achieved in the United States, zoning restrictions and social license problems often make these projects costly and difficult to complete on time. In Mexico, there would likely be an easier path to construction, though social opposition to energy projects has been a growing problem in recent years.

Figure 9. U.S. Natural Gas Production and Exports to Mexico

U.S. Natural Gas Production and Exports to Mexico

It is less obvious where a meaningful agenda can emerge between Mexico and the United States on the issue of climate change. Much will depend on the incoming administration’s attitude toward the Paris Accord and to reducing carbon emissions. However, collaboration between Mexico and the United States on renewable energy goes back a long way and we should expect that meaningful cooperation would continue on this issue. The question of transmission for renewables has already been mentioned, but it would also make sense to consider the creation of agreements between regional system operators in the U.S. Southwest with the CENACE and CFE to overcome intermittency problems and help optimize existing and future renewable resources. The experience of the Midcontinent Independent Systems Operator (MISO) in combining hydroelectric resources from Manitoba with wind power produced in Minnesota highlights the potential for linking Mexican and U.S. resources. Furthermore, the government of California has indicated its desire to continue working on climate and energy issues with Mexico, bringing attention to the potential for ongoing collaboration at the level of U.S. states.

Conclusion

As the Trump administration takes office, the energy relationship between Mexico and the United States is at a historic high point. Mexico’s new energy model, based on market dynamics and attracting private and foreign investment, has opened the way for a highly constructive and productive dialogue between national authorities and their U.S. and Canadian counterparts. Regular meetings of the energy minsters of the three NAFTA countries have helped deepen mutual understanding and further energy cooperation at both the regional and global levels.

Four areas can be added to the existing agenda of energy and climate cooperation. Ensuring Mexico’s continuing status as a “friendly” oil supplier means that the United States has an interest in assisting its southern neighbor to maximize the potential of its oil fields. Second, sharing the successful U.S. experience in energy regulation, and in particular in reducing regulatory burden, will help Mexico succeed and integrate its energy markets. Third, energy infrastructure planning presents an opportunity to coordinate investments across the border to ensure that benefits are optimized for both countries. Lastly, a focus on increasing natural gas production and use in the United States is entirely compatible with the change underway in Mexico. Continued Mexican consumption of cheap gas from the United States will ensure both stable prices and improve Mexican economic competitiveness.

Mexico has an unprecedented opportunity at the beginning of the new administration to build an even stronger energy relationship with the United States. Existing North American cooperation, the progress seen under the energy reform and the interest of the Trump administration in helping the U.S. energy sector to grow provide the ideal platform for a vibrant dialogue on these issues, one that can drive prosperity and employment creation in both nations.

Duncan Wood is the director of the Mexico Institute at the Wilson Center. Prior to this, he was a professor and the director of the International Relations Program at the Instituto Tecnologico Autonomo de Mexico (ITAM) in Mexico City for 17 years.